Claiming Home Office Expenses From 2023

Working from home became widely popular during Covid-19, it was a new experience for most people with dining rooms becoming offices and kitchens the new

Working from home became widely popular during Covid-19, it was a new experience for most people with dining rooms becoming offices and kitchens the new

So you snagged your Christmas gifts and hung the ornaments on your tree, and it’s the early days of December! Now you’re thinking about how

Do you have two jobs? If the answer is yes, then you need to make sure your employer is deducting enough tax from each pay

Many Canadian small businesses that took a hit during the pandemic benefited from the Canada Emergency Business Account (CEBA) interest-free loan in 2020/2021. The program

Over the past couple of months, the most frequently asked questions were: What is instalment interest and how can I avoid it? If you would

At some point in time, either for your business or personal income taxes, you’ve probably needed to pay business taxes to the Canada Revenue Agency

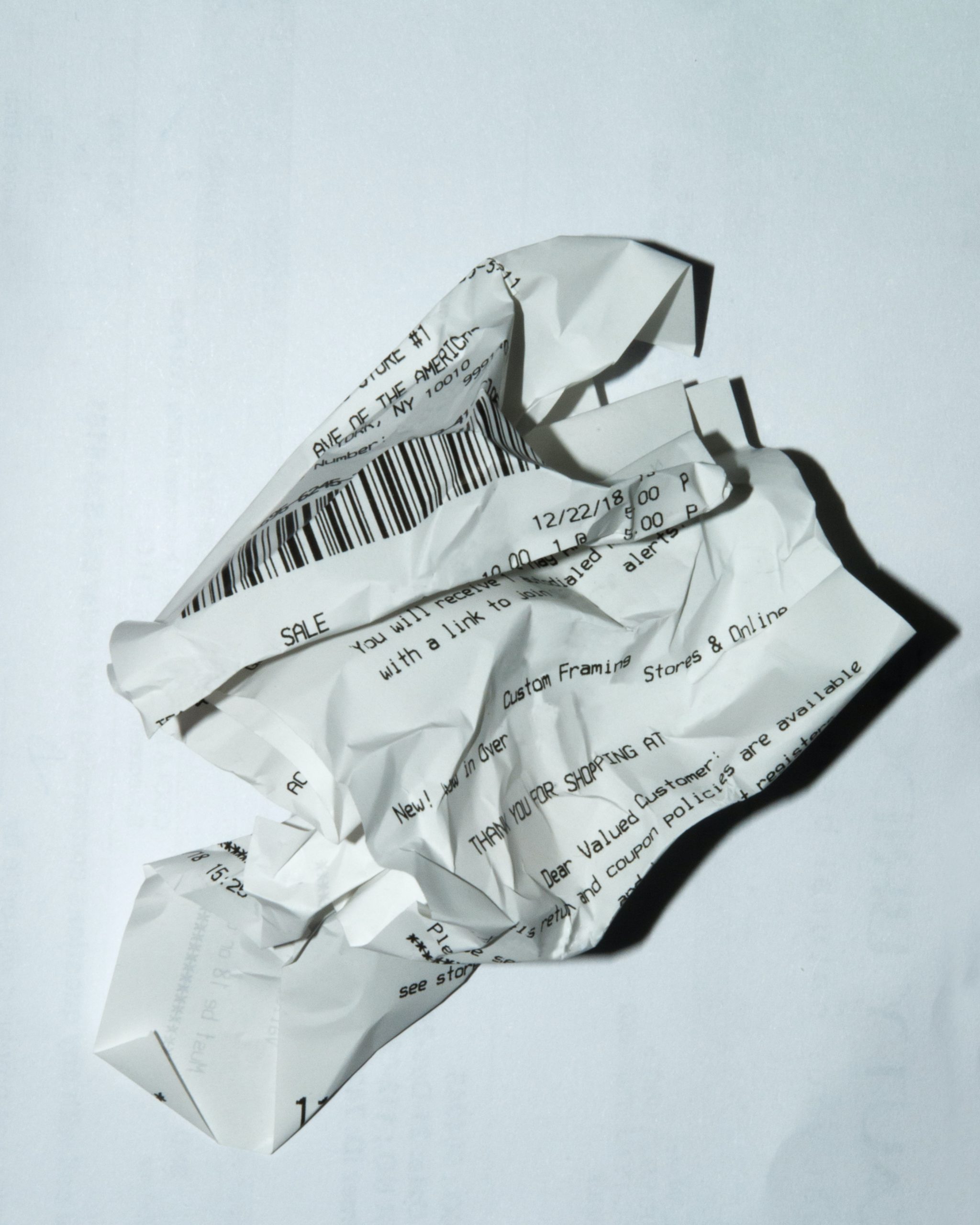

A sad story of a forgotten receipt. Once upon a time, it was a wrinkle-free, crisp piece of paper with dark, glossy lettering. But then

The pandemic has been a very challenging time for businesses around the globe. Frequently changing regulations, social distance requirements, employee and customer safety concerns, and

While the coronavirus has made travelling difficult, it has also created an avenue for more people to work online. We expect to see an increase

Covid-19 has pushed a lot of businesses online and created an unprecedented surge in e-commerce growth. While many consumers are excited to return to in-person